Confused about whether you should put more money into equities (for growth) or fixed income (for stability)? You’re not alone—most working professionals don’t struggle with “what to invest in” as much as they struggle with “how much to put where.” That’s exactly what smart asset allocation solves: it gives your money a clear job—some to grow, some to protect, and some to keep you steady when markets get messy.

What are fixed income investments (in simple words)?

Fixed income is a category of investments that typically pays you a more predictable return compared to equities. You won’t usually get “rocket-like” growth, but you also don’t usually face the same level of ups and downs.

Common fixed income options include:

- Government bonds and Treasury bills

- Bank fixed deposits (FDs)

- Corporate bonds (from companies)

- Debt mutual funds (that invest in bonds)

- Other interest-paying instruments (depending on your country and access)

Think of fixed income like the “shock absorber” in your portfolio. It may not win the race alone, but it helps you stay in the race during bad roads.

Why fixed income feels “boring” (and why that’s good)

Equities can rise fast, but they can also fall fast. Fixed income is usually steadier, which matters a lot when:

- You’re investing for a goal with a deadline (like retirement)

- You want smoother returns year to year

- You don’t want to panic-sell during market crashes

Why asset allocation matters more than picking the “best” investment

Many beginners spend time hunting for the perfect stock or the perfect mutual fund. But for long-term wealth, the bigger driver is often how you split your money across categories—especially equity vs fixed income.

Asset allocation matters because it helps you:

- Manage risk without guessing the market

- Avoid panic decisions when equities fall

- Stay consistent with long-term investing

- Match your investments to your time horizon (how long you can stay invested)

A simple way to understand this: your return comes from taking risk, but your success comes from taking the right amount of risk.

Equity vs fixed income ratio: what it really means

Your equity vs fixed income ratio is simply the split of your investable money between:

- Equity (higher growth potential, higher ups and downs)

- Fixed income (more stable, lower growth potential)

Example splits look like:

80/20: Mostly equity, some fixed income60/40: Balanced approach40/60: More stable, less volatile

There is no “one perfect ratio” for everyone. The right ratio depends mainly on:

- Your age

- Your goal timeline

- Your risk tolerance (how well you handle ups and downs)

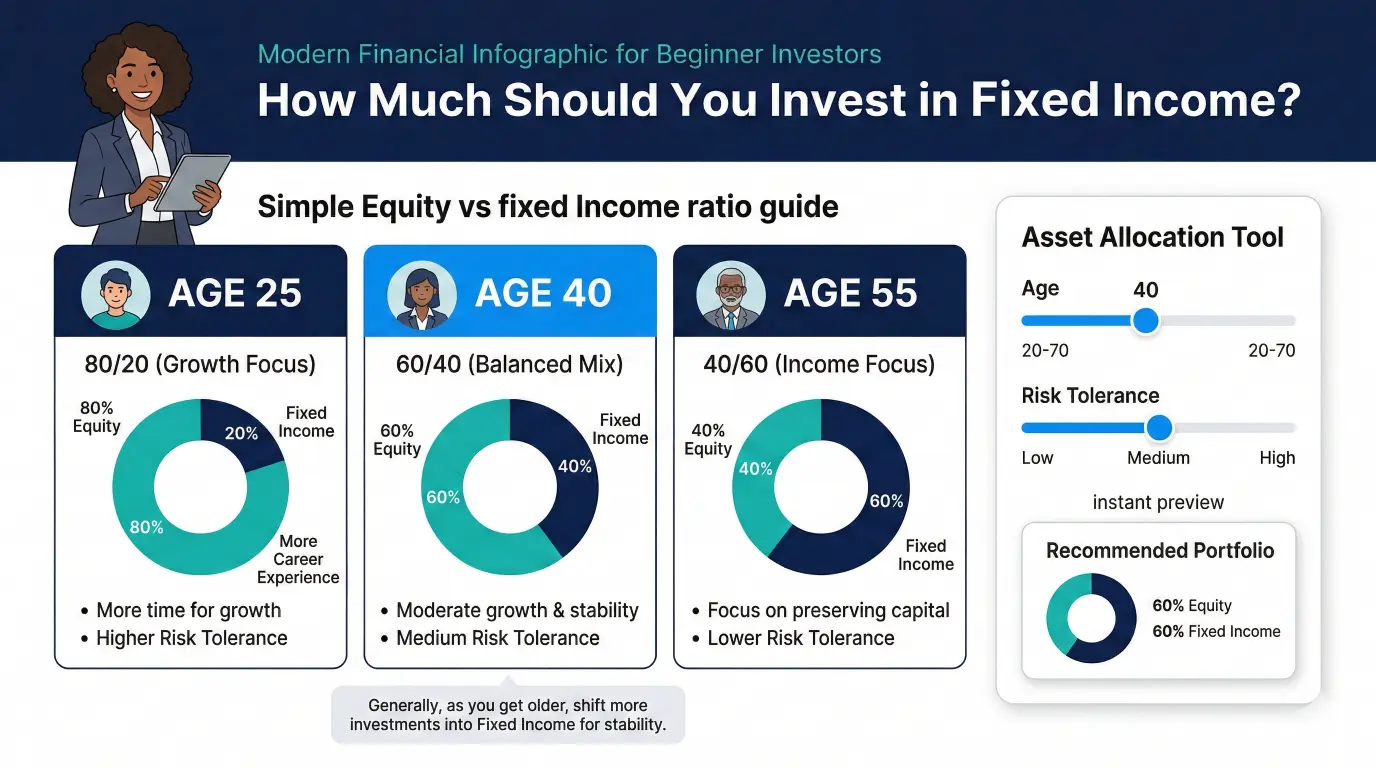

How age affects fixed income allocation (the easiest rule of thumb)

As you get older, you generally have less time to recover from big market drops—so fixed income allocation often increases with age.

Here are simple, beginner-friendly guidelines (not strict rules):

In your 20s and early 30s

You usually have time on your side.

- Equity:

70\%to90\% - Fixed income:

10\%to30\%

In your late 30s to 40s

You still want growth, but stability becomes more important.

- Equity:

60\%to75\% - Fixed income:

25\%to40\%

In your 50s

You’re closer to retirement, so big drawdowns can hurt plans.

- Equity:

40\%to60\% - Fixed income:

40\%to60\%

Near retirement and post-retirement

You often prioritize steady income and capital protection.

- Equity:

20\%to40\% - Fixed income:

60\%to80\%

These are broad ranges. Your personal situation can shift this up or down—and that’s where an asset allocation tool becomes useful.

Risk tolerance: the factor most people ignore (until it’s too late)

Two people of the same age can need very different allocations.

Ask yourself: if your portfolio dropped 20\% in a bad year, would you:

- Stay invested calmly?

- Feel anxious but hold on?

- Panic and sell?

Your honest answer matters more than fancy strategies.

A simple way to map risk tolerance to allocation

- High risk tolerance: Higher equity, lower fixed income

- Medium risk tolerance: Balanced split

- Low risk tolerance: Higher fixed income to reduce swings

If you already know you lose sleep when markets fall, a higher fixed income allocation can actually help you build wealth—because you’ll be more likely to stay invested.

Common allocation strategies (including the classic 60/40)

You’ve probably heard of “60/40.” It’s popular because it’s easy to follow and tends to balance growth and stability.

The 60/40 portfolio

60\%equity40\%fixed income

Why people like it:

- Not too aggressive, not too conservative

- Often smoother than heavy-equity portfolios

- Easier to stick with long-term

Other simple strategies you’ll hear about

80/20 (Growth-heavy)

Best suited when you have:

- Long timeline (10–20+ years)

- High risk tolerance

- Strong ability to stay invested during crashes

50/50 (Balanced and calm)

Often a fit when you want:

- Decent growth with lower volatility

- A “middle path” without extremes

40/60 (Stability-first)

More common when you:

- Have shorter timelines

- Are nearing retirement

- Need lower portfolio swings

These are starting points, not life sentences. The smarter move is to adjust based on your life stage and comfort with risk.

Practical scenarios: how much should you invest in fixed income?

Let’s make this real with simple examples.

Scenario 1: 28-year-old, long-term wealth goal

- Timeline: 25–30 years

- Risk tolerance: Medium-high

Possible allocation: - Equity:

80\% - Fixed income allocation:

20\%

Why it works: you get strong growth potential while keeping a stabilizer for tough years.

Scenario 2: 38-year-old, family responsibilities, medium risk tolerance

- Timeline: 15–20 years

- Risk tolerance: Medium

Possible allocation: - Equity:

65\% - Fixed income:

35\%

Why it works: still growth-focused, but less “roller-coaster.”

Scenario 3: 52-year-old, retirement in 8–10 years

- Timeline: 8–10 years

- Risk tolerance: Medium-low

Possible allocation: - Equity:

45\% - Fixed income allocation:

55\%

Why it works: reduces the risk of a major market fall ruining near-term retirement plans.

The biggest mistake: choosing a ratio once and never updating it

Your allocation should shift as life changes. Common triggers for updating your equity vs fixed income ratio:

- Your age moves into a new decade

- Your income changes significantly

- You take on a big loan or new responsibility

- Your retirement date becomes clearer

- Market volatility reveals your true risk tolerance

Also, your portfolio naturally drifts. If equities perform well, equity can become a bigger percentage than you planned—so you may need rebalancing (bringing the split back to your target).

Use a portfolio allocation calculator (without making it complicated)

Most people don’t need a spreadsheet to do this. They need a quick way to:

- Pick their age

- Select risk comfort level

- See a recommended equity vs fixed income ratio

- Understand “what to do next”

That’s why an online asset allocation tool is helpful: it turns vague confusion (“Should I add more debt funds?”) into a simple, actionable split.

How an asset allocation tool can help

A good tool should let you:

- Calculate equity vs fixed income split based on age

- Adjust allocation based on your risk profile

- Instantly see recommended portfolio distribution

- Use it like a portfolio allocation calculator you can revisit each year

Instead of guessing, you get a clear baseline you can follow—and tweak as your life changes.

Try this: a simple 3-step approach (with the asset allocation tool)

If you want a clean starting plan, do this:

- Decide your goal timeline (retirement, house, education, etc.)

- Choose your risk comfort level honestly

- Use an asset allocation tool to get your recommended equity vs fixed income ratio, then invest accordingly

This keeps it informative-first and decision-friendly, without pushing you into complex products.

Asset allocation tool

If you’re unsure where to start, try the asset allocation tool now to get a personalized equity vs fixed income split based on your age and risk profile. It’s a quick way to see a recommended portfolio distribution in seconds—so you can invest with clarity, not guesswork.

Retirement asset allocation: why this decision matters long-term

Retirement planning fails less because people pick the “wrong fund,” and more because they take the wrong risk at the wrong time.

- Too much equity near retirement can cause large drops right when you need stability

- Too much fixed income too early can slow growth and make your target harder to reach

Smart allocation helps you balance both: growth when you have time, stability when you need safety.

Conclusion: smart allocation beats constant guessing

Fixed income isn’t “wasted money” and equity isn’t “easy money.” They play different roles. When you choose the right fixed income allocation and keep your equity vs fixed income ratio aligned with your age and risk tolerance, you make your plan more stable, more realistic, and easier to stick with—especially during market ups and downs.

If you want an easier way to decide your split today (and revisit it each year), use an asset allocation calculator as your starting point. A clear plan, followed consistently, is one of the most practical advantages a beginner investor can have.

")

")